Pandemics and panics - what are we doing about it?

3 March 2020

Not much... for now.

We are already positioned cautiously because markets are (probably) quite expensive. We have noted how many other low conviction long equity investors are waiting beside the fire exit. So should we get off the equity bandwagon ahead of (or during) the rush? Frankly, we are not sure and we don’t think it’s time to fight the Fed.

Do we even know if the latest sell-off is the start of something bigger?

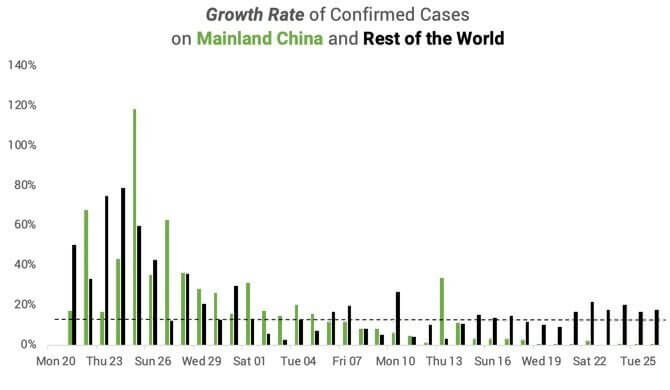

If the numbers coming out of China are to be believed, then the spread of the virus has slowed dramatically within China’s borders. However, it is quite possible (and we have heard it to be the case) that Hubei province has simply not reported for the last few days. The recent flat-lining of the Chinese data could support this thesis, just as it could indicate that the drastic actions of the Chinese authorities have been successful. What we do know is that confirmed cases outside of China have surged but overall remain comparatively low. That means the data is quite lumpy with the Diamond Princess cruise ship, a Church in Korea and a group of small towns in northern Italy having an outsized impact on the data.

Jonathan Ramsay — February 26, 2020

Jonathan Ramsay — February 26, 2020

Listen to the InvestSense Podcast with Andrew Hunt

We have heard from various sources that sustained growth rates in confirmed cases of the virus above 20% are cause for serious concern while rates in the low teens would point to something more manageable. The last few days we saw those levels breached. While it was probably inevitable that we would see an initial ramp-up in cases as the focus moved from Chinese containment to global coping, the media in the Western world has reached fever pitch levels in the last few days. What we don’t know is whether this is another set-back that will ultimately be seen as a buying opportunity or the straw that broke the back of the global economy.

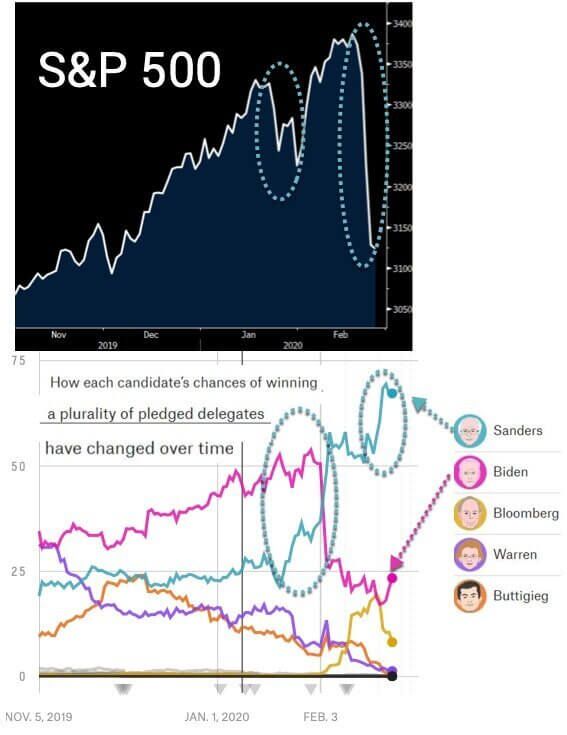

In fact, we can’t even be sure that it is just the Coronavirus that has caused the recent falls in markets (bear in mind that while media headlines make for compelling narratives we still don’t know with absolute certainty what caused the 1987 crash thirty-three years and many books later). One compelling reason, or contributing factor, for recent market turmoil, is the polling of the Democratic Nomination in the US where Bernie Sanders’ standing jumped markedly in recent days vs the more market-friendly Joe Biden. Compared to the unknowns of the Coronavirus, the economic impact of a Sanders Presidency is relatively easy for markets to discount (given the prevailing assumptions of most market participants).

In fact, we can’t even be sure that it is just the Coronavirus that has caused the recent falls in markets (bear in mind that while media headlines make for compelling narratives we still don’t know with absolute certainty what caused the 1987 crash thirty-three years and many books later). One compelling reason, or contributing factor, for recent market turmoil, is the polling of the Democratic Nomination in the US where Bernie Sanders’ standing jumped markedly in recent days vs the more market-friendly Joe Biden. Compared to the unknowns of the Coronavirus, the economic impact of a Sanders Presidency is relatively easy for markets to discount (given the prevailing assumptions of most market participants).

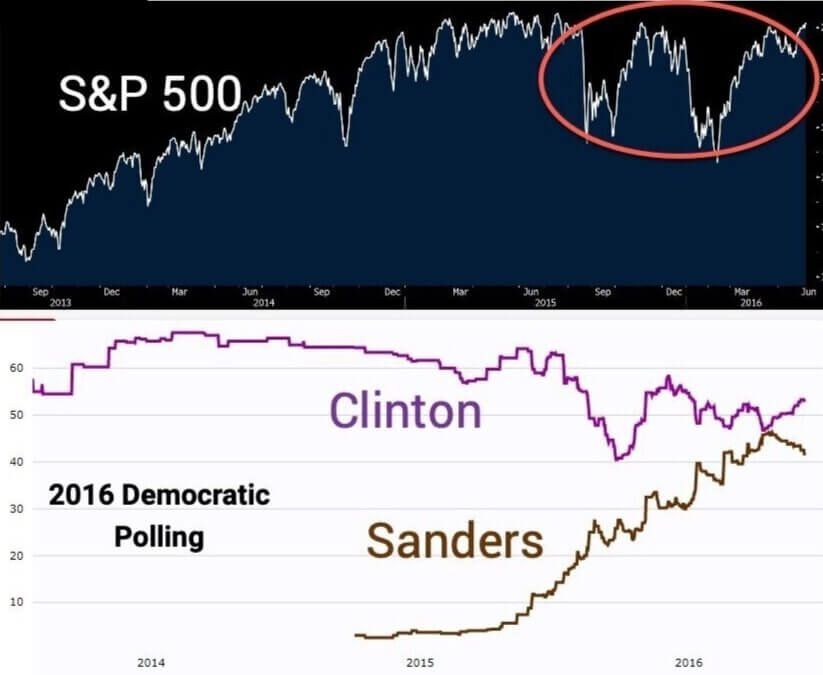

It is, of course, early days in this race but in this respect Bernie has form. It is highly plausible that the last time the US felt the ’Burn’ was not a particularly market-friendly environment, and that was before the world had really contemplated the possibilities of populist policies. This reminds us that markets are volatile precisely because they quickly discount future scenarios, that may or may not happen. Sell the rumour buy the fact?

The market has also spent much of the last 30 years making life difficult for asset allocators and forecasters. The market has fallen by 5% or more 27 times in that period. 12 of those happened during a bear market but these occurrences were concentrated within 5 years (2000-3 and 2007-8). The rest of the time they proved to be feints that left many hapless investors whipsawed and wrong-sided on both the fall and the subsequent rebound. Of course, the time will come (possibly quite soon) when it becomes apparent that we are deep into something bigger but in our view right now there is simply not enough tangible information to convince us to become more defensive than we already are. This is a subjective view which we discussed this evening with Andrew Hunt, who we consider to be more ‘plugged-in’ than ourselves. He too remains on the fence but, absent any further developments, awaits data from the US Federal Reserve on Friday which should reveal the extent to which the US central bank is willing to support markets in the way that the People’s Bank of China evidently has been recently.

Postscript

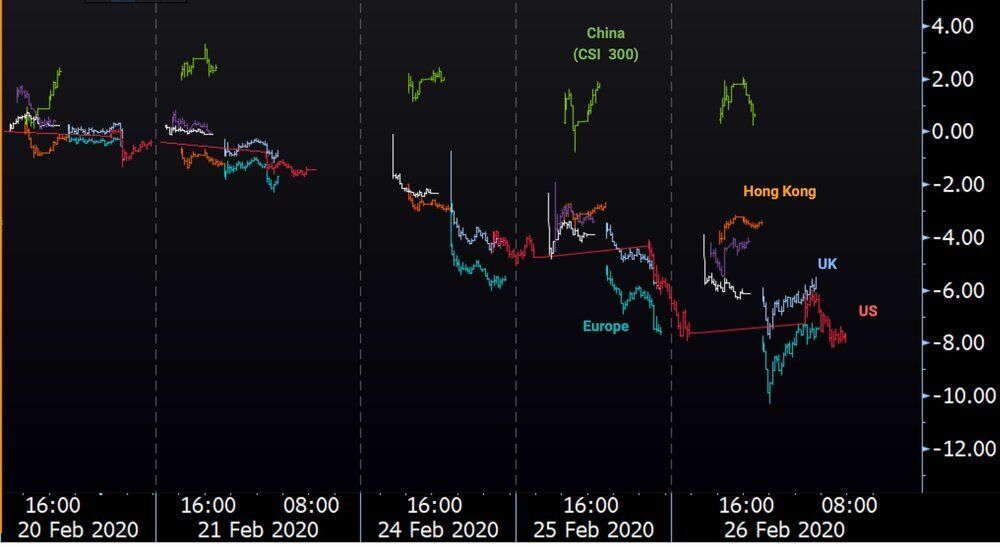

The markets continued their wild swings overnight. Europe plummeted and then mostly recovered while the US then opened up and retraced its steps later on. At times like these, we find these multi-day/intra-day charts useful in interpreting the swings in sentiment and how they shift across the globe. In this one, it is interesting to note that Asia has started to be strangely resilient when compared to the early part of the month. Maybe the focus is shifting to how the Coronavirus will affect the Northern Hemisphere and the West. Or maybe it has indeed more to do with what is happening in the US, or at least the sentiment of US investors?

Latest News

The government has announced it will make some practical changes to its proposed tax changes for people with large super balances (over $3 million) that will now take effect from 1 July 2026.

Big changes are on the way for aged care, with new rules starting from 1 November 2025. While these changes aim to create a more sustainable and fairer system, they do bring added complexity — especially when it comes to understanding the fees and making the right financial decisions. Here are the five key things you need to know: 1. Aged care will cost more - but is still subsidised If you or a loved one is moving into residential aged care from 1 November 2025, the amount you’ll need to contribute will be higher. That said, the Government will continue to fund a large share of care costs - around 73% on average. But it will be important to consider your cashflow. 2. Expect new terminology and fee calculations The language is changing. Instead of the current “means-tested care fee,” you’ll now see new names like Hotelling Contribution and Non-Clinical Care Contribution. How much you are asked to pay will still be based on your income and assets, but new formulae may result in higher contributions than under the current rules. 3. Lifetime caps remain – but at a higher level A lifetime cap will continue to apply to limit how much you can be asked to pay as a non-clinical care contribution over your total stay in residential care. This cap is increasing to $130,000, but with a new safeguard, that no matter how much you pay, you will only need to pay this fee for a maximum of four years. This helps ensure fairness between residents with different levels of wealth. 4. Retention amounts are being reintroduced If you choose to pay a lump sum for your room (known as a refundable accommodation deposit - RAD), aged care providers will deduct a “retention amount” of up to 2% per year (capped at 10% over five years). While this increases the cost slightly, it may still be better value than paying the daily accommodation payment. 5. Good advice can prevent costly mistakes Navigating these new rules can be confusing - especially when you need to make major decisions about the family home, assets or pension entitlements. The cost of getting good advice is often small compared to the cost of getting it wrong. That’s why seeking qualified aged care financial advice is more important than ever. If you're starting to think about aged care for yourself or a family member, now is the time to start planning and seek advice. As specialists in aged care advice, we can help you to make informed decisions with confidence and peace of mind. Please contact Lynde via the link below to chat more about these changes.

Victoria's 'Commercial and Industrial Property Tax Reform' and how this will affect Stamp Duty for these properties is discussed with Principal Solicitor Brad Matthews and host Gavin Nash. Changes are coming on July 1st 2024 in this area and Brad gives us great insight into how and what is changing - and when!

Victoria's 'Vacant Residential Property Tax' is discussed with Principal Solicitor Brad Matthews and host Gavin Nash. Changes are coming on July 1st 2024 in this area and Brad gives us great insight into how and what is changing - and when!